Contura Announces Third Quarter 2020 Results

• Reports net loss from continuing operations of $69 million for the third quarter 2020

• Posts Adjusted EBITDA(1) of $20 million for the third quarter 2020

• Continues strong cost management in all operating segments with historically low CAPP – Met costs

• Reduces long-term debt by approximately $31 million in the third quarter of 2020

• Introduces 2021 guidance

BRISTOL, Tenn., November 9, 2020 – Contura Energy, Inc. (NYSE: CTRA), a leading U.S. coal supplier, today reported results for the third quarter ending September 30, 2020.

(millions, except per share)

| Three months ended Sept. 30, 2020 | Three months ended June 30, 2020 | Three months ended Sept. 30, 2019(2) | |

|---|---|---|---|

| Net (loss) income(3) | $(68.6) | $(238.3) | $(43.6) |

| Net (loss) income(3) per diluted share | $(3.75) | $(13.02) | $(2.29) |

| Adjusted EBITDA(1) | $19.7 | $16.9 | $40.0 |

| Operating cash flow(4) | $(5.9) | $79.0 | $20.4 |

| Capital expenditures | $(27.8) | $(41.5) | $60.3 |

| Tons of coal sold | 5.5 | 5.1 | 5.8 |

1. These are non-GAAP financial measures. A reconciliation of Net Income to Adjusted EBITDA is included in tables accompanying the financial schedules.

2. Excludes discontinued operations, except as noted.

3. From continuing operations. Second and third quarters 2020 no longer have discontinued operations.

4. Includes discontinued operations. Second and third quarters 2020 no longer have discontinued operations.

“Our third quarter results continued to highlight the discipline and safe, strategic performance of our operations team as we achieved the lowest full-quarter CAPP – Met cost per ton performance since the formation of our company,” said chairman and chief executive officer, David Stetson. “As we introduce 2021 guidance, we expect our costs to remain very competitive at our recent levels while we tackle the continued softness in the met coal market and the many uncertainties facing the global economies.”

Financial Performance

Contura reported a net loss from continuing operations of $68.6 million, or $3.75 per diluted share, for the third quarter 2020. In the second quarter 2020, the company had a net loss from continuing operations of $238.3 million or $13.02 diluted share, which included a non-cash asset impairment charge of $161.7 million.

Total Adjusted EBITDA was $20 million for the third quarter, compared with $17 million in the second quarter, primarily due to improved margins in the CAPP – Thermal and CAPP – Met segments.

Coal Revenues

(millions) Three months ended Sept. 30, 2020 Three months ended June 30, 2020

CAPP - Met $295.4 $316.3

CAPP - Thermal $39.8 $36.7

NAPP $64.8 $57.5

CAPP - Met (excl. f&h)(1) $245.6 $261.5

CAPP - Thermal (excl. f&h)(1) $36.8 $32.1

NAPP - (excl. f&h)(1) $62.8 $52.0

Tons Sold (millions) Three months ended Sept. 30, 2020 Three months ended June 30, 2020

CAPP - Met 3.3 3.2

CAPP - Thermal 0.6 0.6

NAPP 1.6 1.3

1. Represents Non-GAAP coal revenues which is defined and reconciled under “Non-GAAP Financial Measures” and “Results of Operations.”

The CAPP – Met revenue decline in the third quarter was driven by an approximately $8 per ton decline in price realizations relative to the second quarter. CAPP – Thermal revenues increased due to higher realized prices. Third quarter NAPP revenues increased as a result of higher volumes, while prices were in line with the prior quarter.

Coal Sales Realization(1)

(per ton) Three months ended Sept. 30, 2020 Three months ended June 30, 2020

CAPP - Met $73.79 $81.61

CAPP - Thermal $57.86 $49.52

NAPP $40.01 $40.19

1. Represents Non-GAAP coal sales realization which is defined and reconciled under “Non-GAAP Financial Measures” and “Results of Operations.”

Global metallurgical coal prices experienced continued softening in the quarter, which resulted in our average CAPP – Met coal sales realization declining 11 percent against the prior quarter to $73.79 per ton. While our 2020 domestic business continues to benefit from annual fixed price contracts, the lower third quarter realizations were primarily driven by our export business, where prices were soft during most of the quarter. The CAPP – Thermal segment experienced higher realization primarily due to improved customer mix.

Cost of Coal Sales

(in millions, except per ton data) Three months ended Sept. 30, 2020 Three months ended June 30, 2020

Cost of Coal Sales $367.3 $383.3

Cost of Coal Sales (excl. f&h/idle)(1) $305.6 $310.5

(per ton) Three months ended Sept. 30, 2020 Three months ended June 30, 2020

CAPP - Met(1) $66.49 $74.41

CAPP - Thermal(1) $45.98 $45.38

NAPP(1) $35.03 $32.98

1. Represents Non-GAAP cost of coal sales per ton which is defined and reconciled under “Non-GAAP Financial Measures” and “Results of Operations.”

In the third quarter, the company reported its strongest full-quarter cost performance in the CAPP – Met segment since the company’s 2016 formation, with CAPP – Met costs averaging $66.49 per ton in the third quarter. The second quarter cost of coal sales was $74.41 per ton, and excluding the impact of April furloughs, incremental one-time COVID-19 mitigation costs, and the partially offsetting benefit from an annual severance tax adjustment, the cost per ton was approximately $70 in the second quarter. The continued cost improvement trend that has been achieved in 2020 is driven by strong productivity growth, labor cost reductions instituted in the second quarter, and improved sourcing.

CAPP – Thermal also continued its impressive cost of coal sales performance, with third quarter cost of $45.98 per ton as compared to $45.38 for the prior quarter. NAPP cost of coal sales for the quarter was $35.03 per ton, up from $32.98 per ton in the second quarter.

Selling, general and administrative (SG&A) and depreciation, depletion and amortization (DD&A) expenses

(millions) Three months ended Sept. 30, 2020 Three months ended June 30, 2020

SG&A $14.5 $12.0

Less: non-cash stock compensation and one-time expenses $(1.0) $(1.9)

Non-GAAP SG&A(1) $13.5 $10.1

DD&A $50.7 $49.3

1. Represents Non-GAAP SG&A which is defined under “Non-GAAP Financial Measures.”

Contura’s third quarter 2020 SG&A expenses were $13.5 million, excluding non-cash stock compensation expense and one-time expenses of $1.0 million, compared with $10.1 million in the prior quarter.

Liquidity and Capital Resources

“We continue to closely manage our cash priorities as prolonged pandemic uncertainty has created additional softness in both end-markets and pricing for our products. As such, we expect fourth quarter capex to come in around $20 million, and we remain focused on continuing the outstanding execution on costs that has allowed us to weather adverse market circumstances,” said Andy Eidson, Contura’s chief financial officer. “We continue to expect to receive the accelerated AMT tax refund of $66 million in the near term. Furthermore, we have filed an NOL carryback in which we claimed approximately $70 million in additional tax refunds. The claim is subject to an IRS audit and we hope to finalize the audit during 2021. All of these items factor into the total liquidity picture for the company, and our philosophy remains one of strategic cash preservation as we close out an unprecedented year and issue guidance and expectations for 2021.”

Cash used by operating activities for the third quarter 2020 was $5.9 million and capital expenditures for the third quarter were $27.8 million. In the prior period, the cash provided by operating activities was $79.0 million and capital expenditures were $41.5 million. Contura continues to anticipate that capital expenditures for the full year 2020 will be in the range of $135 million to $140 million, with 2021 capital expenditures expected to be materially lower in the range of $80 million to $100 million.

As of September 30, 2020, Contura had $161.4 million in unrestricted cash and $180.0 million in restricted cash, deposits and investments. Total long-term debt, including the current portion of long-term debt as of September 30, 2020, was $597.5 million, down approximately $31 million from the prior quarter. At the end of the third quarter, the company had total liquidity of $161.4 million, including cash and cash equivalents of $161.4 million and no remaining unused availability under the Asset-Based Revolving Credit Facility (ABL). The future available capacity under the ABL is subject to inventory and accounts receivable collateral requirements and the achievement of certain financial ratios. As of September 30, 2020, the company had $18.4 million in borrowings and $122.4 million in letters of credit outstanding under the Asset-Based Revolving Credit Facility. In October, subsequent to the quarter close, the company repaid $15.0 million of borrowed principal under the ABL.

2021 Full-Year Guidance

The company is introducing 2021 guidance with coal shipments guidance range of 20.4 million tons to 22.2 million tons, with CAPP – Met segment volume expected to be between 13.5 million to 14.5 million tons with pure metallurgical coal shipments of 12.5 million to 13.0 million tons and thermal shipments in this segment of 1.0 million to 1.5 million tons. CAPP – Thermal segment volume is anticipated to be between 1.3 million tons to 1.7 million tons. NAPP volumes are expected to be in the range of 5.6 million tons to 6.0 million tons.

For 2021, Contura has committed and priced approximately 34% of its metallurgical coal within the CAPP – Met segment at an average price of $86.41 per ton and 72% of thermal coal in the CAPP – Met segment at an average expected price of $52.11 per ton. In the CAPP – Thermal segment the company is 99% committed and priced at an average price of $57.17 per ton and 100% committed and priced for NAPP at an average price of $40.43 per ton.

The company expects our strong cost performance to continue in 2021 with CAPP – Met cost of coal sales per ton anticipated at a range of $68.00 to $74.00. CAPP – Thermal is expected to be in the range of $45.00 to $49.00 per ton and NAPP between $33.00 and $37.00 per ton.

For 2021, the company expects its SG&A to be in the range of $45 million to $50 million, excluding non-recurring items and stock compensation. In light of our decision to forgo certain capital expenditures for NAPP, our overall 2021 capital expenditures guidance at a range of $80 million to $100 million is near the maintenance capital level. Depreciation, depletion and amortization is expected to be between $160 million and $175 million and cash interest expense in the range of $51 million and $55 million.

2021 Guidance

in millions of tons Low High

Metallurgical 12.5 13.0

Thermal 1.0 1.5

CAPP - Metallurgical 13.5 14.5

CAPP - Thermal 1.3 1.7

NAPP 5.6 6.0

Total Shipments 20.4 22.2

Committed/Priced1,2,3 Committed Average Price

Metallurgical 34% $86.41

Thermal 72% $52.11

CAPP - Metallurgical 37% $80.52

CAPP - Thermal 99% $57.17

NAPP 100% $40.43

Committed/Unpriced1,3 Committed

Metallurgical 27%

Thermal 21%

CAPP - Metallurgical 27%

CAPP - Thermal 1%

NAPP --%

Costs per ton4 Low High

CAPP - Metallurgical $68.00 $74.00

CAPP - Thermal $45.00 $49.00

NAPP $33.00 $37.00

In millions (except taxes) Low High

SG&A5 $45 $50

Idle Operations Expense $27 $33

Cash Interest Expense $51 $55

DD&A $160 $175

Capital Expenditures $80 $100

Tax Rate --% 5%

Notes:

1. Based on committed and priced coal shipments as of October 27, 2020. Committed percentage based on the midpoint of shipment guidance range.

2. Actual average per-ton realizations on committed and priced tons recognized in future periods may vary based on actual freight expense in future periods relative to assumed freight expense embedded in projected average per-ton realizations.

3. Includes estimates of future coal shipments based upon contract terms and anticipated delivery schedules. Actual coal shipments may vary from these estimates.

4. Note: The Company is unable to present a quantitative reconciliation of its forward-looking non-GAAP cost of coal sales per ton sold financial measures to the most directly comparable GAAP measures without unreasonable efforts due to the inherent difficulty in forecasting and quantifying with reasonable accuracy significant items required for the reconciliation. The most directly comparable GAAP measure, GAAP cost of sales, is not accessible without unreasonable efforts on a forward- looking basis. The reconciling items include freight and handling costs, which are a component of GAAP cost of sales. Management is unable to predict without unreasonable efforts freight and handling costs due to uncertainty as to the end market and FOB point for uncommitted sales volumes and the final shipping point for export shipments. These amounts have historically varied and may continue to vary significantly from quarter to quarter and material changes to these items could have a significant effect on our future GAAP results.

5. Excludes expenses related to non-cash stock compensation and non-recurring business development expenses.

Operational and Strategic Update

With regard to the Cumberland Mine in Pennsylvania, the company is in active negotiations for the divestiture of the Cumberland property with a potential purchaser. No definitive agreement has been reached at this time, and there can be no assurances that any transaction will result from these negotiations or as to the terms, timing or approval of any such transaction that may be proposed. More information will be announced if an agreement is reached.

Contura has made significant progress in streamlining the enterprise portfolio and incrementally adjusting toward a simplified, more efficient group of mines and plants to better serve the production and sales needs of the company. “Through strategic decisions to idle certain thermal properties in the organization, and by carefully planning how and when to mine out of properties as they come to the end of their expected tenures, we have meaningfully improved both costs and operational efficiencies this year,” said Jason Whitehead, Contura’s chief operating officer. “As mines have come offline, we have been able to realign coal processing into fewer plants, redeploy equipment to other locations across the company, and plan for the best utilization of the newer, high-quality mines in our portfolio. We expect to continue building on this success through the fourth quarter and into 2021.”

Conference Call

The company plans to hold a conference call regarding its third quarter 2020 results on November 9, 2020, at 10:00 a.m. Eastern time. The conference call will be available live on the investor section of the company’s website at https://investors.conturaenergy.com/investors. Analysts who would like to participate in the conference call should dial 866-270-1533 (domestic toll-free) or 412-317-0797 (international) approximately 15 minutes prior to the start of the call.

ABOUT CONTURA ENERGY

Contura Energy (NYSE: CTRA) is a Tennessee-based coal supplier with affiliate mining operations across major coal basins in Pennsylvania, Virginia and West Virginia. With customers across the globe, high-quality reserves and significant port capacity, Contura Energy reliably supplies metallurgical coal to produce steel. For more information, visit www.conturaenergy.com.

FORWARD-LOOKING STATEMENTS

This news release includes forward-looking statements. These forward-looking statements are based on Contura’s expectations and beliefs concerning future events and involve risks and uncertainties that may cause actual results to differ materially from current expectations. These factors are difficult to predict accurately and may be beyond Contura’s control. Forward-looking statements in this news release or elsewhere speak only as of the date made. New uncertainties and risks arise from time to time, and it is impossible for Contura to predict these events or how they may affect Contura. Except as required by law, Contura has no duty to, and does not intend to, update or revise the forward-looking statements in this news release or elsewhere after the date this release is issued. In light of these risks and uncertainties, investors should keep in mind that results, events or developments discussed in any forward-looking statement made in this news release may not occur.

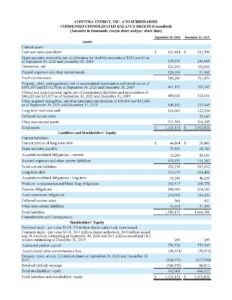

(Amounts in thousands, except share and per share data)

(Amounts in thousands, except share and per share data)

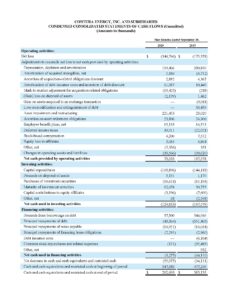

(Amounts in thousands)

(Amounts in thousands)

(In thousands, except for per ton data)

Media Contact

Investor Contact

InvestorRelations@

External Resources

Metallurgical Coal Producers Association (MCPA)

![]()

National Mining Association (NMA) Industry News and Resources

![]()